Banking & Financial Services Industry Reviving Economic Confidence through Policy Relief & Operational Transformation

Banking & Financial Services Industry Reviving Economic Confidence through Policy Relief & Operational Transformation

Once the World Health Organization declared the outbreak of the COVID-19 pandemic, uncertainty and instability among financial service entities became evident. The global financial system is slowly evolving from an initial period of extreme stress, primarily due to government level efforts to stimulate the economy, central banks’ steps towards addressing market disruptions and the resilience of financial institutions. While the initial struggle due to the financial crisis may have eased, firms and policy-makers remain concerned about a range of risks that could prove to be a threat to financial stability and economic recovery.

All stakeholders have consistently highlighted the degree of uncertainty prevalent across financial markets and institutions. There is concern about how badly the virus will affect different countries, duration of containment measures in different markets, how effective policy will be at mitigating lost activity, and how households and firms will change their behaviour in the medium term.

While financial system resilience, fiscal support, regulatory flexibility and liquidity provision to date have helped ensure that the financial system is supportive of economic recovery, a more intensive slowdown may present new risks to the financial system. Thus, while the initial phase of the crisis has eased, participants are keenly aware that there may be greater turmoil affecting the financial system as the economic fallout continues, potentially precipitating a financial crisis down the line. The economic slowdown due to COVID-19 will impact demand for loans which could dent profits for NBFCs among the other financial Service institutions. One view of a global scenario would involve a severe protracted recession in advanced economies leading to a credit crunch, as banks face greater credit losses than their balance sheets can withstand, despite ongoing central bank support which, in turn, would deepen the recession. While this scenario is not seen as likely, equity market investors should be more cognizant of downside risks.

The economic and financial crisis in emerging markets and developing economies could be worse than in advanced economies. Both private-sector participants and policymakers remain concerned about the range of risks presented by weaknesses in many emerging markets and developing countries.

While some emerging markets are better positioned to withstand and address these shocks, many are seeking various forms of liquidity support from advanced economies. There has been record demand for emergency programmes from the International Monetary Fund (IMF) and multilateral development banks, which these institutions have met by expanding the size and structure of the support offered.

Despite the challenging situation, this is also an opportunity for financial institutions to show that they understand their customers’ plight and are committed to supporting them through the crisis. The upside of these difficult circumstances is that they can be used to build stronger, enduring, trust-based relationships with customers.

Short-term liquidity is critical in ensuring confidence in the market forces at play in servicing finance, capital and debt as businesses start adjusting to the rapidly evolving operating environment.

Impact of COVID-19 on the Industry

Within Banking and Financial service sector companies, the short- term impacts in four key areas are:

- Credit Management: Non-Performing Liabilities (NPL) will surge as consumers and businesses are unable to make loan payments and there will be increased demand for new credit. If effective action is not taken, there will be a rapid rise in consumer and commercial NPLs as borrowers struggle to make scheduled interest and principal payments. There will also be a material impact on the auto and equipment finance sectors as borrowers struggle to make lease payments.

- Revenue Compression: Rate cuts as well as a collapse in demand will have a top-line impact. Emergency interest rate cuts to stimulate the economy may lead to net new lending, but will also compress banks’ net interest margin in many markets. Stock market volatility may create a flight to safety to insured deposit accounts, but the pricing on these deposits needs to be addressed quickly to prevent the impact of falling rates from being amplified. While credit, payments and Net Interest Margins are likely to be the primary revenue impacts, no part of the bank will escape a widespread drop in demand that triggers a global recession.

- Customer Service and Advice Provision: Restrictions on personal interactions will push customers toward digital channels for service and sales. Most banks will keep branches open as a vital service. However, customers are being told to minimize in- person interactions and stay home, so many will look to manage their financial life through apps, online banking and greater reliance on their bank’s contact centre.

- Operating Model Adjustments and Cost Control: Misaligned revenues and cost will require banks to improve operational flexibility and rethink short-term priorities. Because of the cumulative impact of the pandemic-driven factors, there will inevitably be a misalignment of short-term costs and revenues in the banking sector for at least the next few quarters. As a matter of urgency, banks need to review and prioritize project expenditures and assess what can be slowed/ stopped and what can be redirected to initiatives with short-term impact, such as improving digital servicing capabilities or building a loan modification workflow for call centres.

Risks associated with the above impact areas include market risk associated with a sharp drop in interest rates and increased volatility in securities and FX price, counterparty credit risk with the current market events affecting counterparty credit profiles, non-financial risks such as conduct risk, culture and model risk, third party risk and cyber risk, risk governance, dividends and stock buybacks along with risks in credit ratings with market induced negative environment impacting banks and stakeholders, especially in the high-yield grade.

Operational resilience in crisis readiness, communications, monitoring and review, flexibility, quality and productivity is critical to overcome the crisis and be ready to address future crises.

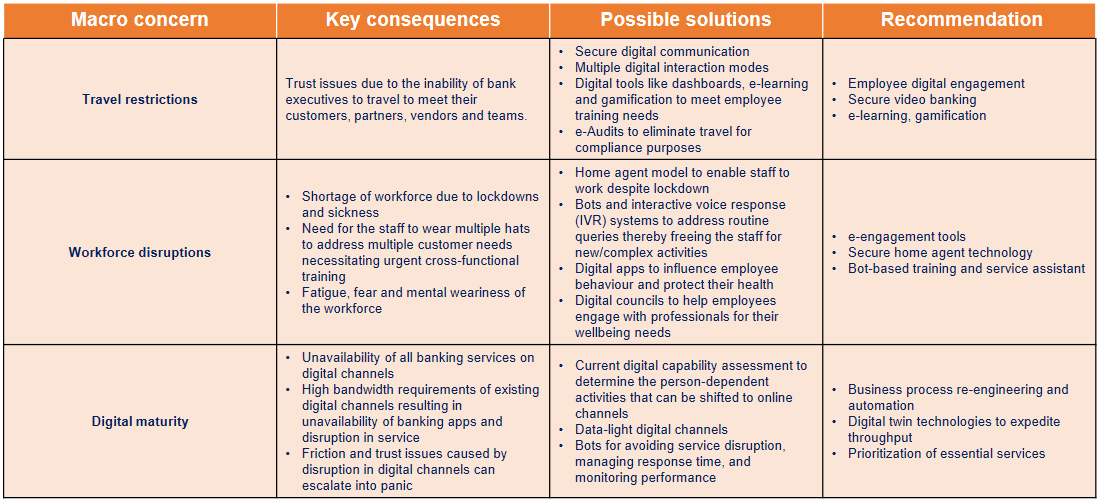

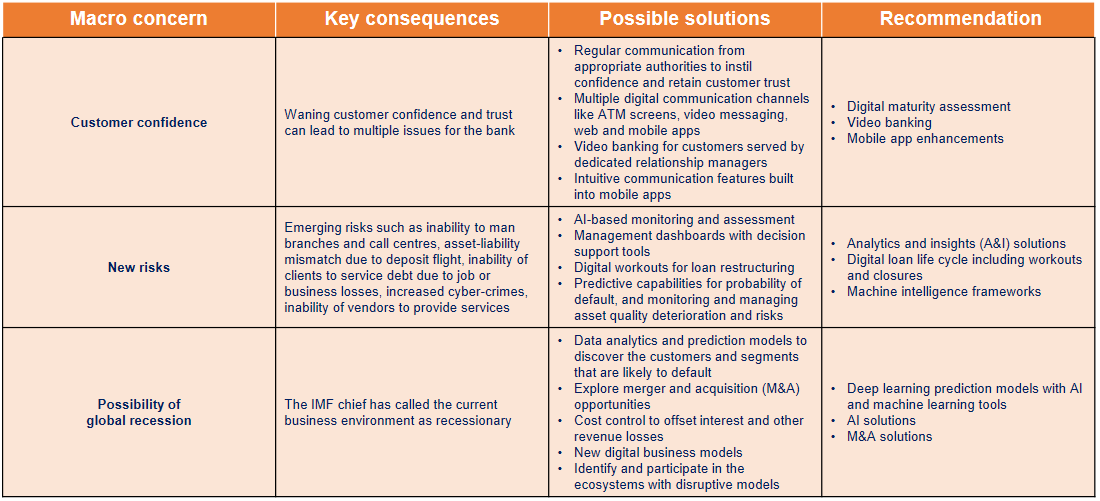

Impact Assessment and Recommendations (1/2)

Impact Assessment and Recommendations (2/2)

Policy Relief for Reviving Economic Confidence

Flattening the curve of firm mortality must be the top policy priority, and governments need to expand the size and scope of support programmes over time. To prevent short-term liquidity problems from becoming solvency issues, governments must remain vigilant about the availability of funds for SMEs and larger firms as the crisis persists. Moreover, given that SMEs have short windows of cash on hand, programmes must be designed to ensure rapid disbursement of funds through simple, all-digital channels. As the economic crisis unfolds, it will be necessary for the government to provide support to so-far-excluded companies, such as middle-market firms lacking access to capital markets.

Governments, including regulators and central banks, must continue to coordinate policy on a global level to help maintain financial stability. Within countries, policy guidance must be clear and consistent across regulatory agencies. While regulatory policy within countries has generally moved in the same direction, in certain areas, regulators and supervisors are not sufficiently harmonized in their approach. Policy-makers should ensure that regulatory and supervisory changes are coordinated across the relevant domestic institutions to prevent confusion from limiting the effectiveness of policy action.

Policy-makers must ensure that the financial system remains capable of safely meeting the public’s need for financial services through digital channels. Given the need to quickly disburse

fiscal support to households and small businesses – in addition to the broader need to deliver financial services at a time when populations are being asked to socially distance – financial institutions must have leading digital capabilities. However, the crisis has so far exposed the variation in digital maturity among institutions.

In the short term, policy-makers should leverage the strengths of the entire financial system, including FinTech, to rapidly deliver support to small businesses and households. Moving forward, banks can explore partnerships with FinTech to quickly and safely introduce new products. Policy-makers should also encourage banks to continue to explore other technologies and partnerships that enable them to better serve digital-first customers and to operate in a more agile fashion. Given increased reliance on e-commerce and contactless payments, policy-makers should continue to explore technologies that enable fast, inexpensive, and ubiquitous payments through a resilient payment system.

Advanced economies may need to further expand the support offered to emerging markets and developing economies. Advanced economies have moved to increase their support to emerging markets and developing countries through both bilateral and multilateral channels; but, as the crisis in these countries unfolds, additional assistance may be required. Advanced economy policy- makers, as well as investors and financial institutions, must continue to develop and expand programmes to support these countries.

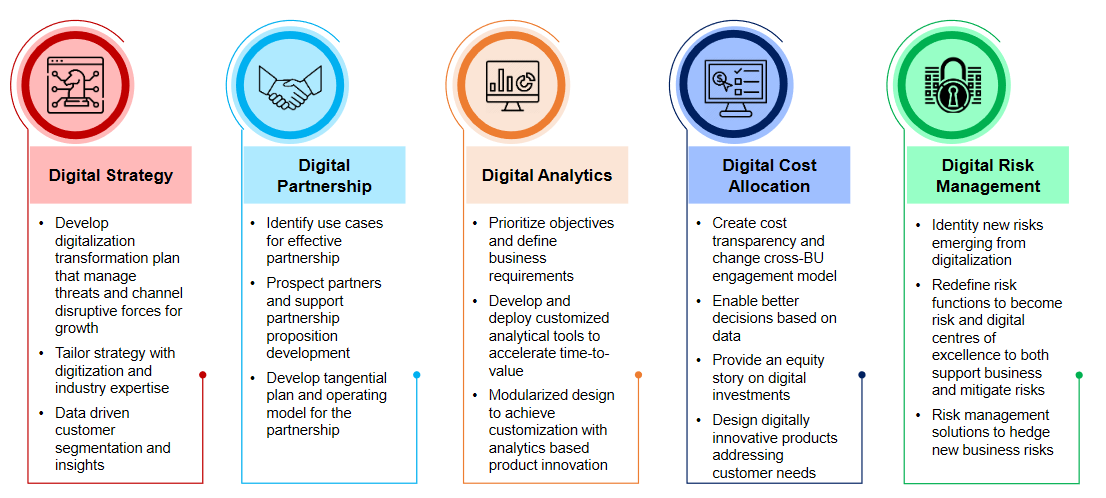

Digital Acceleration towards a Disruptive Operational Model

Industry Outlook – The Indian Perspective

Like any previous episode of economic slowdown, the most immediate fall-out of this pandemic was felt on the Financial Services sector. This is the reason why the Reserve Bank of India (RBI) came out with a Rs 3.74 trillion of support that enveloped most sectors. Additionally, the RBI cut the interest rate at which it lends to banks by 75 basis points. The other key measure announced was the forbearance on payment of instalments on all sorts of loans including farm loans. This will apply to all loans offered by regional rural banks, small finance banks and local area banks, co-operative banks, scheduled banks, and NBFCs (including housing finance companies and micro-finance institutions).

The measures are meant to ease disruptions in fund flows to real sectors of economy, avoid working capital shortage for businesses and stem panic withdrawals by households from banks and nonbanking deposit-taking institutions. The confidence building measures have also had a positive impact on outflows of capital by foreign institutional investors (FIIs) as well as drying up of external commercial borrowings. The move to reset working capital loans will particularly provide support to SME financing, averting significant distortion of supply chains.

Despite the RBI package, Indian banking and financial sector faces tough challenges in the coming months. Some sectors of economy such as travel, hospitality and transportation & logistics are badly hit. Credit exposure of commercial banks and nonbanking financial companies to those sectors may gradually turn into bad assets in the coming days.

The assessment of COVID-19-related dislocation in Indian financial sector can be studied from two angles: firstly, the channels that would perpetuate the risks already built up over the past few months, and secondly, the new challenges emanating from global economic shocks in the form of falling foreign direct investment (FDIs) and collapse of export revenues, remittance flows, etc.

Following the first strand, despite noticeable improvement in banking segment in terms of capital adequacy, liquidity and asset quality after seven years of deterioration, Indian banking is not entirely free from challenges. Overhang of NPAs and low credit growth by scheduled commercial banking indicates build up of risks in the system which may deteriorate further if cut in aggregate demand and business activity prolongs. The second channel of risks for Indian banking and financial sector is the contagion from faster transmission of global shocks.

All these developments would help aid the slowdown to worsen in a synchronized fashion thereby impacting commercial banking. Higher allocation of government expenditure towards fighting corona virus manifested in the form of medical supplies and health infrastructure would cut or postpone capital expenditure in other sectors to a great extent. In order to sustain efforts directed towards COVID-19, Indian financial sector needs to be prepared for tougher times in the coming days.

Reputation Challenges for the Industry

These are testing times and banks will need to quickly initiate measures to ensure seamless delivery of services to customers with minimal disruptions. Solutions that provide rapid or quick resolutions to the problems created by the COVID-19 crisis are the need of the hour. In most scenarios, short and crisp interventions must be initiated to carefully tread this slippery road. Navigating the COVID- 19 landscape will pose tough challenges to financial institutions, and collaborating with a trusted service provider is proving to be the way forward.

Reputational risks and opportunities have increased manifolds triggered by the uncertainties of Covid-19 pandemic for the BFSI enterprises.

There is an urgent need to consider the multiple near-, short-, and medium-term operational, financial, risk, and regulatory compliance implications. The situation has presented many opportunities to support market and economic activity and to facilitate a quick return to stability. If banks and capital markets firms respond well to these unprecedented challenges, they will not only help society, but also increase trust and the reputation of the banking industry in the long run.

cost of reputation risk is difficult, in part because it can arise as a consequence of other operational risks. A large number of firms especially the micro, small and medium businesses and also self- employed individuals are likely to default on their bank and NBFC loans. With these external challenges, Financial organisations ought to guard against reputation risks by a sizeable investment in process thinking and cultural improvements as they can result in huge losses to the institutions. Institutions should view risk management as an institutionalisation of best business practices, so as to anticipate risk events, minimise their impact and profit from it.

Areas of focus in reputation management could stem out of the existent operational capabilities and shortcomings, digital divide, customer demography ease of access and quality of service provided. There is a clear divide between established and emerging markets in the perceptions of digital versus traditional financial service providers where digital transformation has increased financial inclusion, one third of consumers believe digital providers are more trustworthy. In the digital age, data security and honesty are also leading concerns when engaging with financial services companies. It is imperative to create a culture of treating reputation risk seriously through integrity and collaboration.

Consocia Advisory, has been at the forefront of building and protecting organisational and brand reputation for several sectors.

We remain available to curate effective programs to pre-empt and mitigate risks through process-thinking, process-improvement and institutionalisation of best business practices, so as to anticipate risk events, minimise their impact and safeguard the overall future of the enterprise.

Cushioning the COVID impact on our clients: Consocia’s value driven services providing dynamic solutions

As COVID-19 grew into a global crisis, Consocia realized the need to support industry colleagues in dealing with the biggest challenge faced ever in recent times that of business continuity. In response to the situation, we were swift in curating an in-house crack team comprising experts in research and insights; stakeholder database generation; content; government relations and public policy.

Consocia Advisory engaged Central and State Governments besides many Districts through strategic narrative backed by data to highlight the need of the hour in the fight against the deadly pandemic. We urged immediate orders to restore Client’s ability to manufacture, warehouse, transport and distribute the client’s essential products across the country.

Presently, Consocia is working with several enterprises for business continuity as well as crisis management. In the last few weeks, we have helped opening of plants and warehouses of the Indian entity of a global disinfectant company in 6 states including in Red zones as well as

Containment areas, besides that of a renowned lighting solutions company in two states (Haryana and Karnataka) already while they are now looking for our assistance in three more states.

Within a few days of being on-boarded, through our 24×7 support, we were able to secure not only policy interventions for manufacturing but also for warehousing, logistics and distribution as well as access to staff & workers. In the process, we were able to assure the Central and State Government stakeholders that all due precautions are being taken to prevent and contain COVID 19. We even helped with internal SOPs for transportation and staff movement.

We are helping the apex body representing the Shopping Malls across India against the debilitating impact the Coronavirus pandemic has had on them. On behalf of SCAI, Consocia has crafted several interventions to draw the attention of the stakeholders and policy-makers on the plight of the industry and reinforcing reasons for Malls to be considered for resuming operations in a staggered manner, for the post-lockdown phase. At the same time, Consocia is working with the empowered Group of Ministers and Committees for COVID-19 response as well as the RBI seeking urgent financial stimulus for the sector and amplifying the initiatives through media engagement from time to time.

The upcoming editions of the dynamics of business transformation white paper series will focus on specific industries with strategies and outcome driven solutions to positively impact business outlook for business recovery and continuity in the COVID-adjusted world.

COVID-19 is a long battle for the industry. As your trusted well-wisher, our team is available to support you during these uncertain times in the areas of business continuity planning, public affairs, public policy and government relations. Contact us: reachus@consociaadvisory.com